IEFA Blog

International Student Loans

Repayment Period – Why it matters to you?

International student loans are a popular topic of conversation, especially for those students looking for additional financing. While there are many lenders that loan to international students, each loan has its own terms and conditions that will influence how much you pay over the life of your loan. In our previous blog, we defined what…

International Education

IEFA Relaunch

Just when you thought the leading resource in international education financial aid couldn’t get better, it did. IEFA.org has recently had a facelift that includes new additions along with multiple updates to existing features making it a complete resource for finding the aid you need overseas, all in one spot. IEFA has a new, polished look, but the main…

International Student Loans

Private Student Loans for International Students

If you are an international student interested in coming to the United States to study, or if you are currently enrolled in a US university or college, you may be looking for private sources of funding. While scholarships, grants and fellowships are a great place to start, you may soon realize that this is insufficient…

International Scholarships

Scholarships, Grants, Loans, oh my!

If you are planning to study overseas, you may find that going to school in a foreign country can be costly. While you will still have to cover your tuition, books, and living expenses, now you’ll need to factor in additional flight costs, exchange rates, health insurance, etc. While there is no doubt that studying…

International Student Loans

Principal and Interest Rate Defined

As we head into the new academic year, many international students will be looking at international student loan options. Comparing loans is not easy, especially with bank terminology. One of the most important terms that will effect students is how much you are going to pay back over the course of your loan. Loans are…

International Student Loans

Loans for Spring Semester

It’s that time of year again! Many of you have enjoyed your winter vacation filled with holiday cheer and New Year celebrations. As you head back for Spring semester, you may realize that your holiday money did not exactly match the tab for your education. If this is your case, you may consider loans for…

International Education

International Student Loan Comparison Tool

As more students decide to study overseas, financial aid plays a critical role for many students looking to make this a reality. Financial aid comes in many forms, including scholarships, grants, and loans. For many international students, even with the assistance of scholarships and grants, there is still a need to secure additional financing by…

International Education

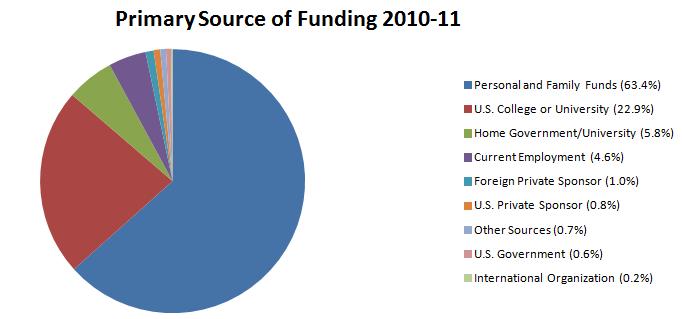

Funding for International Students

Funding for international students is a critical factor for any student looking to receive a degree or certification overseas. Think about it. Housing, food, tuition, and books are just a few of the necessary expenses students will need to consider when they budget for their education. One way students reduce their costs is by applying…

International Education

Interest Rates Still Low on International Student Loans

One positive by-product of a relatively weak ecomony is the continuing low interest rates for international student loans for study in the USA. Interest rates for loan programs offered by International Student Loan range from 2.25% APR to 9.11% APR with no origination fees. When you consider that there is no collateral required for a…

International Student Loans

International student loan available

Student loans are available for international students studying at approved schools in the United States and Canada. There are multiple international student loan programs available – today we will highlight the main two. These loan programs are designed to help students cover the total cost of attendance, including tuition, room and board, and other expenses. International…

Find My Student Loan

Find a LoanRecent Posts

Recent Comments

- on Strategies for Financing your International Education

- on Three Things All International Students Should Know about Financing Their Education

- on Engineering Scholarships for College Students

- on The essential guide to sources of university funding for international students

- on Health Insurance Plans for International Students: Finding the Right Plan for You

Archives

- January 2025

- December 2024

- November 2024

- March 2024

- January 2024

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- November 2018

- October 2018

- September 2018

- July 2018

- May 2018

- March 2018

- January 2018

- December 2017

- November 2017

- October 2017

- August 2017

- July 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- August 2010

- May 2010

- April 2010

- March 2010

- January 2010

- November 2009

- September 2009

- August 2009

- July 2009

- January 2009

- November 2008

- September 2008

- August 2008

- July 2008

- April 2008

- February 2008

- January 2008

- November 2007

- October 2007

- September 2007

- July 2007

- May 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

Categories

- Budgeting Tips for International Students

- Credit Cards

- Financial Aid

- Health Insurance

- International Education

- International Financial Aid News

- International Scholarships

- International student loan refinancing

- International Student Loans

- Off campus employment

- Scholarships

- Study Abroad

- Study Abroad Loans

- Study in Canada

- Study in Germany

- Study in Spain

- Study in the UK

- Study in the USA

- Uncategorized

- Work in the USA

Search

Register to Find Your Perfect Scholarship/Loan

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse tempus vehicula tortor vel tincidunt. Morbi ut varius nunc, vel elementum.

Get the Financial Aid Newsletter