IEFA Blog

International Financial Aid News

Find A Student Loan in 10 Seconds – LIVE, ON AIR

If you are like most international students right now, you are probably scratching your head wondering how you are going to cover your education expenses. After all, tuition alone will cost you thousands and thousands of dollars. And, who has that money at their disposal? If you need more money to help cover this year’s…

International Scholarships

Question 1 of the Financial Aid Fun Contest Released!

Financial Aid Fun Contest: Question 1 Deadline: July 9th at 3pm EST International Student Loan and International Student have combined forces during the month of July to bring you three great chances to win $100! Yesterday the Financial Aid Fun contest was announced and today question 1 of the Financial Aid Fun Contest released! All…

International Student Loans

Student Loan Terms Confusing? Join Us Live This Thursday!

International student loan terms are confusing. Repayment, deferral, interest rate, cosigner, credit score, and the list goes on and on. It’s almost that time to apply for international student loans, and we’re here to help you every step of the way. As you make these important financial decisions, you will need to know what these…

International Financial Aid News

Learn About International Student Loans – Live!

If you need an international student loan for the semester, you have a few more months to prepare! That’s why tomorrow, Wednesday, at 3pm EST, International Student Loan will be hosting a free Google Hangout to answer all of your questions. Join them to learn about international student loans including: What you need to apply…

International Financial Aid News

Come Hangout With Us This Friday: Finding A US Cosigner

If you are looking to apply for a student loan to help finance your education, then you’ll need to have a US cosigner. All international students and most US students need a cosigner to join their student loan application in order to get a US student loan. That’s because these banks and lenders need to…

International Education

Search International Scholarships for Free Money

December is here! And before you head off for winter break, it’s important to also think about your finances. Set a few hours each day searching for awards and applying so that you’ll be in good shape in time for the new semester. Our Scholarship Search makes it easy to do, here’s how: Register Create…

Budgeting Tips for International Students

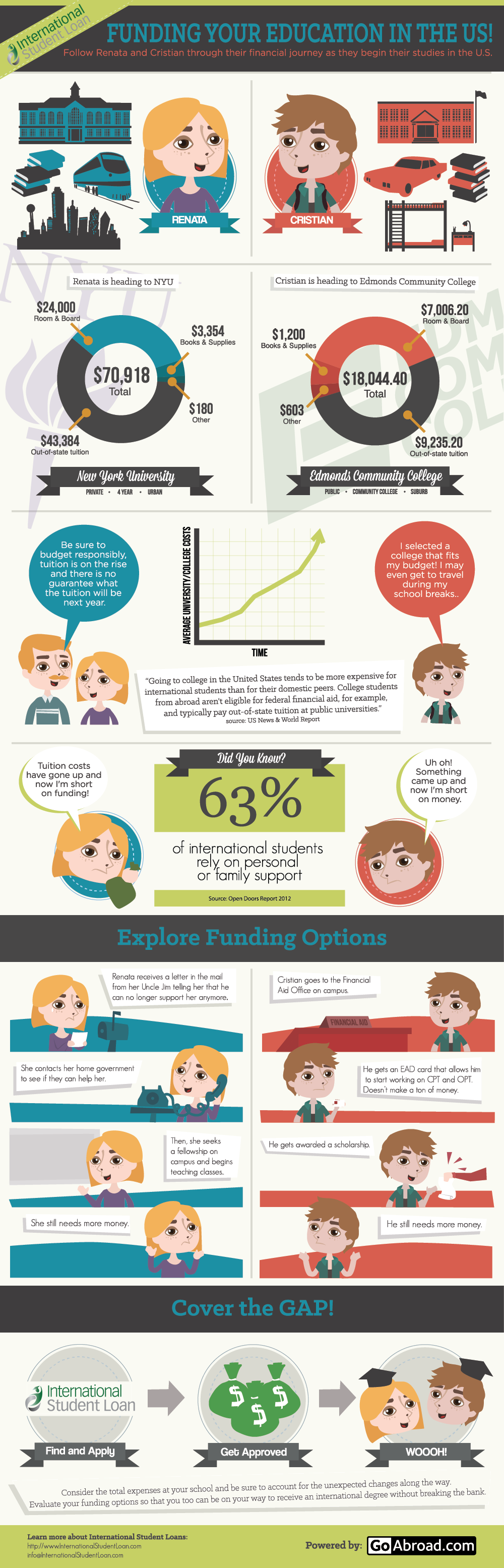

Funding Your Education in the US

As an international student in the US, chances are you have to worry more about funding your education in the US than your domestic peers do. Because international students do not qualify for federal loans and often have to pay out of state tuition at state colleges, they generally end up paying more for their…

International Student Loans

Now Is The Time – Apply for Student Loans

The new school year is almost here and while you may know where you are planning to study abroad – and perhaps even know what classes you’ll be taking – you may soon realize that you still have to get your finances in order. After all, the amount of financial aid available to international students…

International Student Loans

Student Loan Repayment Explained

If you are planning to apply for student loans come July or August, it’s important to know key terms so that you can evaluate lenders and choose the one that works best for you. The international student loans that are available have different repayment options. Repayment is defined as the act of paying back the…

Budgeting Tips for International Students

When Are Student Loans Disbursed?

Students going to college in the United States may be partly paying their way student loans, using them for everything from tuition and room and board to books and supplies. But the exact time for student loan disbursement, as important as it is, can be hard to pin down. So when are student loans disbursed?…

Find My Student Loan

Find a LoanRecent Posts

Recent Comments

- on Strategies for Financing your International Education

- on Three Things All International Students Should Know about Financing Their Education

- on Engineering Scholarships for College Students

- on The essential guide to sources of university funding for international students

- on Health Insurance Plans for International Students: Finding the Right Plan for You

Archives

- January 2025

- December 2024

- November 2024

- March 2024

- January 2024

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- November 2018

- October 2018

- September 2018

- July 2018

- May 2018

- March 2018

- January 2018

- December 2017

- November 2017

- October 2017

- August 2017

- July 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- August 2010

- May 2010

- April 2010

- March 2010

- January 2010

- November 2009

- September 2009

- August 2009

- July 2009

- January 2009

- November 2008

- September 2008

- August 2008

- July 2008

- April 2008

- February 2008

- January 2008

- November 2007

- October 2007

- September 2007

- July 2007

- May 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

Categories

- Budgeting Tips for International Students

- Credit Cards

- Financial Aid

- Health Insurance

- International Education

- International Financial Aid News

- International Scholarships

- International student loan refinancing

- International Student Loans

- Off campus employment

- Scholarships

- Study Abroad

- Study Abroad Loans

- Study in Canada

- Study in Germany

- Study in Spain

- Study in the UK

- Study in the USA

- Uncategorized

- Work in the USA

Search

Register to Find Your Perfect Scholarship/Loan

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse tempus vehicula tortor vel tincidunt. Morbi ut varius nunc, vel elementum.

Get the Financial Aid Newsletter